Architecting resilient, scalable industrial systems in 2026

March 23, 2026Industrial IoT (IIoT) is becoming the digital backbone of manufacturing, energy, utilities, and commercial real estate. Between 2023 and 2026, the market has expanded rapidly, driven by automation, AI integration, and next-generation connectivity such as 5G and advanced edge networks. For industrial leaders, the conversation has shifted from “Should we deploy IIoT?” to “How do we architect it correctly to ensure long-term resilience, security, and ROI?” Connectivity is at the center of that question. Devices, gateways, sensors, controllers, and cloud platforms must operate as a coherent, secure system rather than as disconnected components.

Let's take a deeper look at the state of the Industrial IoT market, the evolution of connectivity technologies, and the architectural principles for building scalable industrial systems.

The state of the industrial IoT market

Industrial IoT has entered a mature growth phase. Market research firms report consistent upward momentum, though total market size varies by scope and methodology. According to Business Wire, the global IIoT market is estimated to grow from $147.2 billion in 2023 to $391.8 billion by 2028, at a compound annual growth rate (CAGR) of 21.6% from 2023 through 2028. These variations reflect differences in how analysts define IIoT, including whether it encompasses software platforms, connectivity, edge hardware, or broader automation ecosystems.

What remains consistent across reports is directionality. Growth is driven by three structural factors: digital transformation of legacy industrial assets, increasing automation requirements, and integration of AI-driven analytics into operational processes. IIoT accounted for approximately 24% of total IoT revenue in 2023, underscoring its weight within the broader IoT economy. Manufacturing alone accounts for roughly 20-28% of the IIoT end-use share, reflecting the sector’s heavy investment in automation, predictive maintenance, and real-time production visibility.

Source: IoT Analytics

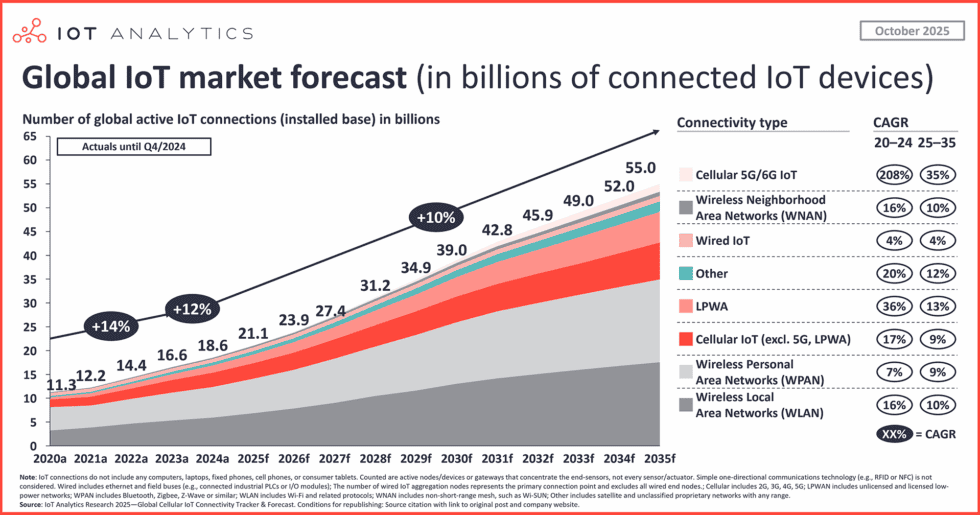

At a macro level, total connected IoT devices reached approximately 21.1 billion at the end of 2025, reflecting 14% year-over-year growth. Projections for 2024 suggest 18.5 billion connected devices globally. While not all are industrial, the scale of device proliferation reinforces a key reality: connectivity architecture is becoming a strategic risk factor. As networks scale, poorly designed systems amplify security vulnerabilities, latency bottlenecks, and operational complexity.

Connectivity technologies: Wi-Fi, 5G, and beyond

Connectivity is the circulatory system of Industrial IoT. In 2023, Wi-Fi accounted for approximately 31% of IoT connections globally, while Bluetooth and cellular IoT technologies together accounted for roughly 80%. Each connectivity option carries trade-offs in bandwidth, latency, reliability, cost, and coverage, and selecting the right combination requires alignment with operational requirements rather than technology trends.

Wi-Fi remains dominant in facility-based deployments due to cost efficiency and ease of integration. It is well-suited for smart building sensors, energy meters, and many industrial monitoring devices. However, Wi-Fi networks may struggle in high-interference or large outdoor industrial environments without careful design. Bluetooth, particularly Bluetooth Low Energy (BLE), is widely used for short-range, low-power sensor applications. Cellular IoT technologies, including LTE-M and NB-IoT, provide extended coverage and improved reliability for distributed assets such as pipelines, remote substations, and fleet equipment.

5G introduces a new tier of industrial capability. Global 5G IoT connections were approximately 17 million in 2023 and are projected to exceed 100 million by 2026. The value of 5G lies not simply in speed, but in ultra-low latency, network slicing, and improved reliability. These characteristics enable use cases such as real-time robotics control, augmented reality-assisted maintenance, and high-density sensor environments in smart cities and advanced manufacturing plants. However, 5G adoption requires careful evaluation of infrastructure costs, spectrum availability, and integration with existing operational technology (OT) systems.

Edge computing and real-time intelligence in industrial environments

As device counts increase and connectivity options diversify, sending all data directly to the cloud becomes inefficient and, at times, impractical. Edge computing addresses this challenge by processing data closer to the source – at gateways, controllers, or localized servers – reducing latency and bandwidth costs while improving resilience.

Industrial environments often require real-time or near-real-time responses. For example, in manufacturing, anomaly detection on a production line must occur within milliseconds to prevent defects or equipment damage. In energy management, load-balancing decisions may need to be executed instantly to avoid peak penalties or grid instability. Relying exclusively on centralized cloud processing introduces latency and dependency on uninterrupted connectivity. Edge intelligence allows local decision-making while still synchronizing aggregated data with cloud systems for analytics and long-term optimization.

The rise of AI integration further strengthens the edge. Machine learning models can now be deployed on gateways and industrial controllers to enable predictive maintenance, quality assurance, and adaptive control systems. Instead of reacting to failures, industrial systems can anticipate them based on vibration patterns, temperature deviations, or usage anomalies. This shift from reactive to predictive operations significantly reduces downtime and improves asset lifespan. However, edge deployments introduce complexity. Devices must be securely managed, firmware updates must be orchestrated across distributed fleets, and data models must remain consistent across environments. A robust IIoT architecture ensures that edge and cloud components operate within a unified governance framework rather than as isolated systems.

Industrial IoT in smart buildings and energy management

Industrial IoT growth is not confined to heavy manufacturing. Smart buildings and commercial real estate increasingly rely on IIoT architectures to improve operational efficiency, energy optimization, and occupant experience. Sensors for indoor air quality (IAQ), HVAC performance, lighting systems, and occupancy monitoring generate continuous data streams that require secure, scalable connectivity.

The expansion of edge computing and 5G networks enhances building-level intelligence. Real-time monitoring enables dynamic HVAC adjustments based on occupancy patterns. Energy management systems can optimize consumption in response to time-of-use pricing or grid signals. Predictive maintenance models detect anomalies in chillers, boilers, or air-handling units before costly breakdowns occur. These capabilities align with broader sustainability mandates and ESG reporting requirements, where transparent data collection and auditability are critical. Manufacturing remains a dominant IIoT segment, but smart buildings represent a rapidly expanding adjacent domain. The same architectural principles apply: secure connectivity, interoperable protocols, scalable device management, and reliable data pipelines. Industrial IoT supports not only automation, but also decarbonization strategies by providing granular visibility into energy consumption and operational inefficiencies.

Designing secure, scalable industrial connectivity architectures

Connectivity scale introduces risk. As device counts climb into the billions globally, poorly designed architectures increase exposure to cyber threats, operational disruptions, and compliance failures. Industrial environments face unique challenges because they blend legacy operational technology (OT) with modern IT systems. Security strategies must therefore address both domains simultaneously.

A resilient IIoT architecture typically incorporates the following principles:

- Segmented network design separating IT and OT domains;

- Encrypted communication protocols across device, edge, and cloud layers;

- Centralized device identity and lifecycle management;

- Secure over-the-air (OTA) firmware update mechanisms;

- Continuous monitoring and anomaly detection across connectivity layers.

Each principle mitigates systemic risk rather than addressing isolated vulnerabilities. Network segmentation limits lateral movement in the event of a breach. Encryption protects sensitive operational data. Device identity frameworks prevent unauthorized endpoints from joining the network. OTA updates ensure that vulnerabilities can be patched without costly site visits. Continuous monitoring provides visibility into abnormal traffic patterns or device behavior. Scalability is equally critical. Industrial deployments often begin with pilot projects but must eventually support thousands or millions of endpoints. Architectures must accommodate growth without requiring a complete redesign. Cloud-native platforms, modular edge components, and API-driven integrations enable expansion while maintaining operational continuity. Governance and compliance are also central to EEAT-aligned best practices. Industrial leaders increasingly operate within regulated environments where data sovereignty, privacy, and operational transparency are mandatory. Designing IIoT connectivity with compliance in mind, rather than retrofitting controls later, reduces long-term risk and cost.

Conclusion

For enterprises, connectivity is a strategic infrastructure that determines whether AI models can operate effectively, whether predictive maintenance reduces downtime, and whether smart buildings achieve energy-efficiency targets. Secure, scalable architectures enable resilience and long-term ROI, while fragmented deployments amplify risk. Industrial IoT success depends on deliberate design choices: hybrid connectivity models, integrated edge intelligence, secure device lifecycle management, and governance frameworks aligned with operational realities. Organizations that treat connectivity as an architectural discipline – rather than a collection of technologies – will be positioned to scale confidently as IIoT continues its rapid evolution. Industrial connectivity is not simply about linking devices. It is about creating intelligent, adaptive systems capable of sustaining industrial performance in an increasingly automated, data-driven world